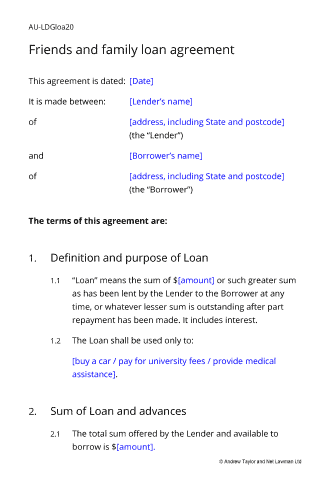

Friends and family loan agreement

Document overview

ACT

ACT NSW

NSW NT

NT QLD

QLD SA

SA TAS

TAS VIC

VIC WA

WA

- Length:4 pages (650 words)

- Available in:

Microsoft Word DOCX

Microsoft Word DOCX Apple Pages

Apple Pages RTF

RTF

If the document isn’t right for your circumstances for any reason, just tell us and we’ll refund you in full immediately.

We avoid legal terminology unless necessary. Plain English makes our documents easy to understand, easy to edit and more likely to be accepted.

You don’t need legal knowledge to use our documents. We explain what to edit and how in the guidance notes included at the end of the document.

Email us with questions about editing your document. Use our Lawyer Assist service if you’d like our legal team to check your document will do as you intend.

Our documents comply with the latest relevant law. Our lawyers regularly review how new law affects each document in our library.

About this loan agreement

Lending money to friends and family can be difficult.

The advantage of borrowing from friends or family members is that the lender is likely to know the borrower well and give better and more flexible repayment terms, such as a lower interest rate than a bank, early repayment or repayment holidays.

It can be uncomfortable to suggest recording the loan in a document.

You may consider a verbal agreement, which technically is legally binding. However, the terms may be unenforceable unless you can prove what they were.

A standard written agreement in a legalistic style may seem too formal given your relationship with the other person. It may prompt questions of trust in your relationship.

However, there are advantages of a written agreement.

It acts as a record as to what was agreed: when the money should be repaid and with how much interest, whether the loan is a gift or an investment. As such, it is more difficult to dispute what was agreed (a benefit for both the borrower and the lender), the parties are more likely to stick to the agreement, and it can help reduce the fears of other family members and friends that somehow the loan is unfair or exploitative.

This simple loan agreement, designed specifically for a loan to a friend or family member, aims to bridge the gap between not using an agreement at all, and using a longer, more comprehensive one.

Written in plain English and keeping length to a minimum, it allows you to record the loan terms in a legally binding contract that doesn't seem to question the integrity of the borrower but which does allow you to take action against the borrower if he or she doesn't pay you on time, or uses the loan for a reason not agreed.

When to use this agreement

Use this agreement when you want to record the loan, but where you have a high level of trust with the borrower.

This agreement could be used for long-term or short-term lending to a friend or family member, as examples: to buy a car, for a deposit on a home, to fund higher education or for an event such as a marriage.

Loan arrangements could include repayment in a single lump sum, or according to a repayment schedule. Charging interest is optional.

Either party may be abroad or in the Commonwealth of Australia, and the loan can be of any size.

This template contains no provisions for security or for a guarantor. If you need these, look at our other loan agreement templates or see the most likely alternatives below.

If you have already given the loan funds to the borrower, you use this document as a retrospective agreement.

Loans against property

In order to keep this agreement straightforward, the lender has no security on the principal.

If you are lending for a deposit on a first home, you might consider securing the loan on the property by lodging a mortgage. A mortgage allows the lender to take possession of the property and sell it if the borrower defaults.

You should note that the bank lending the mortgage is unlikely to agree to do so if there is already an existing mortgage on title. They will want the first mortgage - the first right to take possession.

If the bank doesn't consent to a second mortgage, then you might consider lodging a caveat in place on the borrower's property. The caveator has no more protection than other lenders if the borrower becomes bankrupt, but if there is a caveat, the borrower cannot sell the property without the caveator’s consent.

You can use this loan agreement and subsequently lodge a caveat.

Ensuring the loan is a loan and not a gift

In Australia, a loan is presumed to be a gift if there is no loan agreement. That is another reason to have clear evidence of the arrangement.

When lending to family and friends, this particularly presents an issue on death - whether of the lender or the borrower.

If the lender dies and the loan is considered a gift, then the amounts that each beneficiary of the Will receives might be different to that which the lender expected.

Repayment of the loan funds might be forgiven (since they were a gift), reducing the size of the residuary estate to be shared among other family members.

Or, gifts made within the lifetime of the lender may be deducted from the gifts made through the Will. The borrower may receive less than intended.

If the borrower dies, and if the loan is considered a gift, it may not be repaid. The executors have a legal duty towards the beneficiaries of the estate over honouring an 'informal arrangement' of ad-hoc payments to a family member.

While large family loans could be recorded in a Will, it is usually better to do so in a 'letter of intent'. While it is always best to make clear to the executors and family members that the loan exists, where the loan agreement can be found, and that the arrangement is not a gift, amending a Will does involve work and doesn't change the legal status of the loan or the gift.

Protect against non-repayment in bankruptcy or in divorce

If the borrower is made bankrupt, you might be one of the creditors expecting to have your loan repaid. This will be more likely to happen if there is a formal legal agreement in place.

Likewise, if the borrower's relationship with their spouse or partner breaks down, you'll want to make sure that the court takes into account your loan as part of the couple's assets and liabilities. A written agreement will make sure that a family loan is subtracted from the assets of one or both, and that your son- or daughter-in-law does not claim your money as their own in family law proceedings.

Alternatives to this document

If you need a more comprehensive agreement, but are happy for the loan to be unsecured, see our standard unsecured loan agreement.

If you need a guarantor, then see our agreement that is secured by guarantee.

The law in this document

There is little specific statutory law relating to personal lending, so you are free to agree the terms you want with the borrower. We give you options for different situations.

Drawn outside the National Consumer Credit Protection Act 2009, this agreement is not suitable for companies in the business of lending or providing credit to consumers.

Do you need to obtain independent legal advice?

There is no legal requirement to obtain your own legal advice - whether you are the lender or the borrower. Solicitors will always recommend that you do because a loan can have unintended knock-on effects in other areas of your life.

The contents of the agreement

- Definition and purpose of the loan

- Sum of the loan and advances

- Repayment conditions

- Interest payable

- Miscellaneous legal matters

This template is supported by drafting notes that explain how to edit it for your loan. Our layout and use of plain English make it very easy to edit by deletion.

Recent reviews

Choose the level of support you need

Document Only

This document

This document - Detailed guidance notes explaining how to edit each paragraph

Lawyer Assist

- This document

- Detailed guidance notes explaining how to edit each paragraph

- Unlimited email support - ask our legal team any question related to completing the document

- Review of your edited document by our legal team including:

- reporting on whether your changes comply with the law

- answering your questions about how to word a new clause or achieve an outcome

- checking that your use of defined terms is correct and consistent

- correcting spelling mistakes

- reformatting the document ready to sign

All rights reserved